Workers’ Compensation insurance is required in the majority of states for businesses with employees. It provides several benefits to employees for work-related injuries or illnesses. Benefits include medical treatment, covering the cost of doctor visits, hospital stays, medication, and surgeries if needed; wage replacement up to a certain amount; compensation for a permanent disability; rehabilitation; and death benefits to dependents if the on-the-job injury results in the employee's death.

Workers’ Compensation premiums are based on the type of work employees perform (job classification codes), the company’s total payroll, and its claims history, reflected in the experience modification rate (ex-mod). Higher-risk job classifications and larger payrolls typically lead to higher premiums, while a strong safety record and lower claims frequency can help reduce costs.

There is an audit at the end of the year to reconcile the estimated premium paid at the start of the policy period against the actual payroll figures for that year. Since premiums are initially calculated using projected payroll numbers, the audit ensures the business has paid the correct amount, resulting in either an additional payment owed to the insurer or a refund issued to the business if payroll came in lower than estimated.

The audit is not optional. It is a contractual obligation built into your policy.

In this article, you will learn the importance of the audit, what’s involved in an audit, and how to prepare for an audit.

Why the Workers' Comp Audit Is Important for Contractors

For contractors, payroll can fluctuate significantly from one year to the next. A slow winter, a large commercial project, or the addition of several new crew members can dramatically shift your labor costs. Because your Workers' Comp premium is tied directly to payroll, the end-of-year audit is the mechanism that keeps everything square with your insurance company.

If you underestimated payroll at the start of the policy period, you'll owe an additional premium after the audit. On the flip side, if work slowed down and you ran less payroll than expected, you may receive a refund.

Beyond the financial reconciliation, the audit also ensures your employees are classified correctly. Misclassified workers are one of the most common and costly audit surprises contractors face.

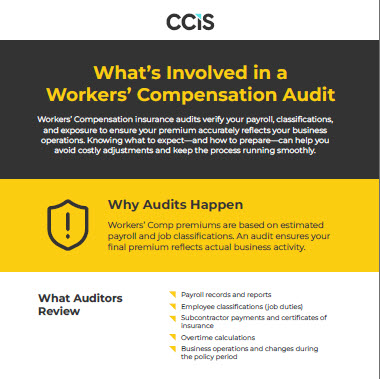

What's Involved in a Workers' Compensation Audit

The audit is typically conducted annually, at the end of your policy period. It may be performed in one of three ways: a physical audit (an auditor visits your place of business), a voluntary audit (you submit records directly to the insurer), or a phone audit (a representative walks you through the process over the phone).

During the audit, the insurance company will review several key records:

- Payroll records. This includes all wages paid to employees: hourly workers, salaried staff, and in some cases, owners or officers of the company. Overtime pay is typically included, although some states allow overtime to be excluded above a certain threshold. Be sure to check your state’s specific rules.

- Certificates of Insurance from subcontractors. This is critical for contractors. If you hired subcontractors during the policy period, you must provide valid Certificates of Insurance showing they carried their own Workers' Compensation coverage. If you cannot provide these certificates, the insurer may add the subcontractors' labor costs to your payroll and charge you as if they were your own employees. This can result in a substantial and unexpected audit bill.

- Job classification codes. The auditor will verify that your employees are classified under the correct codes for the work they actually performed. For example, a roofing laborer and an office administrator carry very different risk levels — and very different rates. If workers were performing higher-risk tasks than their classification reflects, the auditor may reclassify them, increasing your premium.

- Overtime and excluded payroll. Certain types of pay, such as severance or employer contributions to benefit plans, may be excludable from your auditable payroll. Keeping detailed records helps ensure you're not paying premiums on dollars that should be excluded.

How to Prepare for Your Workers' Comp Audit

The best time to prepare for your annual audit is throughout the year. Here’s what you should be doing consistently:

- Collect certificates before work begins. Every time you bring on a subcontractor, require a current Certificate of Insurance before they set foot on the job. Create a simple tracking system to log expiration dates and follow up on renewals. Chasing down paperwork after the audit notice arrives is stressful and sometimes impossible.

- Keep clean, organized payroll records. Your payroll journal and tax records (such as quarterly 941 filings, your annual 940, and Form W-3, which summarizes all employee W-2 forms submitted to the Social Security Administration) are fair game during an audit. If you use payroll software, make sure your reports are easy to run and clearly organized by employee and job type.

- Separate payroll by classification. If your employees perform multiple types of work — some office, some field — keep detailed records of time spent in each role. This allows you to apply the lower classification rate to the appropriate hours, which can meaningfully reduce your premium.

- Review your ex-mod each year. Your experience modification rate is recalculated annually based on your claims history compared to other businesses in your industry. A single large claim can raise your ex-mod and drive up premiums for years. Maintaining a strong safety program, promptly reporting injuries, and proactively managing claims are strategies that protect your ex-mod over time.

- Work with your insurance agent. Your agent should review your estimated payroll at the start of each policy period and update it mid-term if your business grows or contracts significantly. Staying close to your actual payroll reduces the likelihood of a large audit bill at the end of the year.

For contractors who stay organized, consistently collect subcontractor certificates, and keep accurate payroll records throughout the year, the audit is simply a routine confirmation that everything lines up. Understanding what the auditor is looking for and preparing accordingly helps put you in control of your insurance costs.

Frequently Asked Questions

Q. Do I have to buy Workers’ Compensation if I don’t have employees?

A. Typically, Workers’ Comp insurance is mandatory for businesses that have employees. Check with your state’s individual requirements.

Q. Does CCIS provide Workers’ Compensation insurance?

A. Yes, we can provide you with a policy quote so you can protect your business and employees. Contact CCIS for a free quote.

Q. What if I don’t purchase Workers’ Comp coverage?

A. In states where Workers’ Comp is required for businesses with employees, failing to buy coverage can lead to severe consequences, including significant fines, mandatory business stop orders, personal liability for employee medical bills, and potential jail time. Uninsured employers may also face lawsuits from injured workers for negligence and may lose common legal defenses.

Be Prepared

Download our guide to see what’s involved in a workers' compensation insurance audit

Be Prepared for Workers’ Comp Audit

Workers’ Compensation audits are standard, but they can still catch business owners by surprise. Knowing what to expect—and how to prepare—can help you stay compliant, avoid unexpected costs, and keep your premiums under control. Download our infographic to review what’s involved in an audit.

*NOTE: The insuring agreement in a policy sets out the covered perils, assumed risks, and nature of coverage that the insurance company provides to its insured in exchange for the premiums paid. Thus, the terms and conditions of the policy will dictate whether coverage exists and the nature of any potential benefits.