Contractors can once again apply for financial assistance through the Paycheck Protection Program (PPP). The most recent COVID-19 relief package that went into effect on December 28, 2020, allotted an additional $284 billion to fund the program. While many of the logistics remain the same, there are significant updates contractors need to know:

Eligibility: PPP loans in round two are only available to the following businesses:

- Businesses that employ 300 or less employees (reduced from 500).

- Businesses that exhausted all funds received from the first PPP borrow.

- Businesses that experienced gross receipts during Q1, Q2 or Q3 in 2020 that were at least 25 percent less than the same quarter in 2019.

Maximum Loan Amount: Businesses applying for a second PPP loan have two options to calculate its potential maximum loan amount. The first is to multiply the business’ total average monthly payroll in the one-year period prior to the start date of the new loan by 2.5x. The second is to multiple the total average monthly payroll for 2019 by 2.5x. However, businesses applying for a second loan may not borrow more than $2 million (reduced from $10 million) regardless of whether either of the above calculations exceed $2 million.

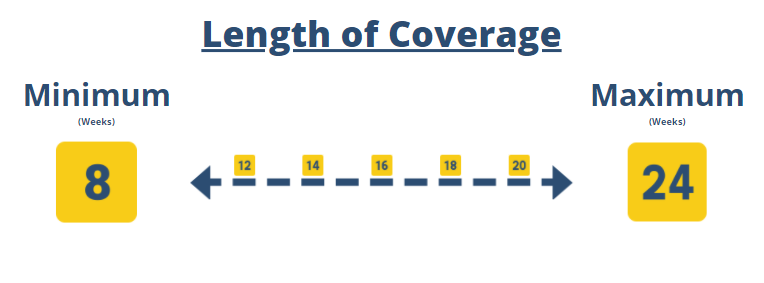

Length of Coverage: The SBA mandated the original length of coverage for a PPP loan was an eight-week period beginning the date a borrowing entity received funds. This period was later extended to 24 weeks to allow businesses to elect for an 8-week or 24-week coverage period. Under the newest conditions, borrowers may now choose a length of coverage consisting of a minimum of eight weeks but does not exceed 24 weeks, retroactive to the date funds were received. This means instead of having to choose between an 8-week or 24-week coverage period, businesses can elect for coverage for any amount of weeks between that range.

Businesses should refer to finances from 2020 to assist in determining the most beneficial length of coverage.

Usage of Funds: Previously, in order to qualify for 100% loan forgiveness, PPP funds had to be used for payroll, rent, covered mortgage interests and utilities. Now, PPP resources may also be allocated to the following expenses:

- Operation expenses (software expenses, inventory, processing, HR functions, etc.)

- Supplier costs (payments to suppliers of items essential to operations)

- Property damage (costs related to damages not covered by insurance)

- Worker protection costs (costs related to CDC, HHS, OSHA regulations, etc.)

Taxes: PPP loans will not be included as taxable income and expenses paid with funds of a forgiven loan are now tax-deductible. This covers not only loans from round two but existing and prior PPP loans.

Contractors looking to apply for PPP assistance should reach out to the bank their business has established a relationship with. If said bank is not affiliated with the program, use the SBA’s Local Assistance Finder to locate and contact one that does.

For information relevant to round one of the PPP, visit our previous post: https://www.ccisbonds.com/content/86-the-paycheck-protection-program-your-financial-lifeline-during-covid19.htm